Weekly Newsletter

Cotton Market Weekly Highlights

Weekly Cotton Market Update – Week 1, 2026

Cotton Market Weekly Highlights

Cotton’s policy levers flipped twice in one week , at the border and at the mill gate. Imports have just become pricier, while yarn realisations and margins appear set to soften in H2 FY26. Here’s what happened in cotton and textiles this week

Cotton import duty snaps back from Jan 1:

India’s duty-free cotton import window ended without an extension, so a 11% duty applies from January 1, 2026. The report cites ICAC saying India imported 36 lakh bales till mid-September (Brazil 23%, US 20%, Australia 19%); farmers in Vidarbha were below MSP ₹8,110/quintal at ~₹7,500–₹7,700 (as low as ₹6,700) while CCI procured 61.5 lakh bales by Dec 30 and MSP registration was extended to Jan 16. For import-reliant mills, the article highlights a cost increase (imports are ₹4,000 more expensive than domestic at ₹58,500/bale). At the same time, farmer groups view the duty as supportive of MSP-linked price realisation. Expect mills to lean harder on domestic/CCI cotton in the near term as import economics worsen.

₹1,100 crore sought for post-harvest upgrades:

CITI reports the Ministry of Textiles is set to receive ~₹1,100 crore (US $ 122 million) from the Mission for Cotton Productivity, over 20% of a proposed ~₹6,000 crore (US $ 668 million) outlay over five years. The funds are intended for ginning/pressing modernisation, lint quality controls, and better bale handling, but releases depend on final Cabinet approval, which the note says has been delayed. If executed, this targets contamination and quality losses that directly hurt cotton’s value at the mill gate and push import dependence. This suggests mills may see tighter bale quality discipline, reducing discounts and improving cotton competitiveness, once approvals unlock spending.

ICRA flags H2 FY26 yarn realisation pressure:

ICRA (via Fibre2Fashion) expects US tariff impacts on Indian apparel exports to moderate cotton yarn realisations in H2 FY26 after a flattish H1, with spinners’ FY26 revenues seen down 4-6% and margins down 50–100 bps. It notes domestic cotton fibre prices fell ~3% MoM in Nov 2025, while average cotton yarn prices fell 4%, taking contribution to ₹96/kg in Nov 2025 from ₹103/kg in H1 FY26, with ₹98–100/kg expected for FY26 (sample: 13 companies, ~25–30% of industry revenue). That squeeze tightens mills’ appetite to pay up for cotton even if arrivals are steady, because yarn pass-through is weakening. Net-net, expect more cautious cotton buying and stricter working-capital discipline from spinners until export-linked demand stabilises.

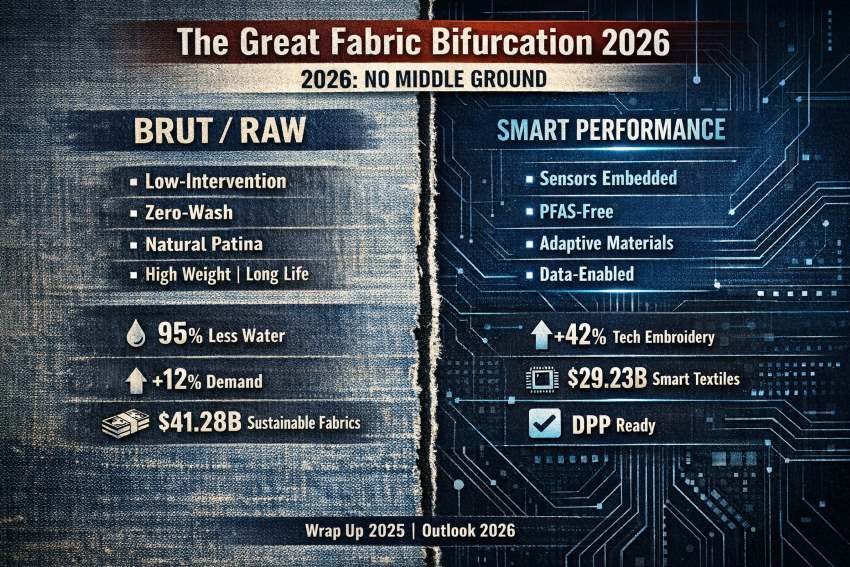

2026 splits: “Brut” naturals vs performance tech:

FashionatingWorld frames 2026 as a dual-track market: rising demand for “Raw/Brut” low-intervention textiles alongside expanding “Smart Performance,” citing a 12% increase in demand for low-intervention textiles and up to 95% lower factory water use by skipping stone-washing/chemical distressing. It also projects sustainable fabrics at $134.7 billion by end-2026 (12% CAGR), recycled polyester at $10 billion, and a 42% surge in technical embroidery. It says the EU DPP registry becomes operational mid-2026, alongside a claimed $1.6 billion India push into technical textiles (56% new entrants in “Clothtech/Protech”).

For cotton, “Brut” aesthetics can reward cleaner, less-contaminated lots and lower-processing finishes, while DPP-linked trade raises the bar on traceability in cotton supply chains. This suggests cotton programs that pair contamination control with DPP-ready data will be better positioned for EU-bound premiums even as performance MMF investment rises.

© 2026 Cotton Guru. All Rights Reserved. | Designed by AdvertSneak Technology